There was a time when conversations about investing in Africa started and ended with oil, gas, and minerals. That story is changing rapidly. Africa is now firmly on the radar of long-term investors not because of its ground-level resources, but because of what is growing above the surface: a young population, expanding cities, a digital economy accelerating faster than most analysts predicted, and governments that are increasingly open for business.

The shift from resource-focused narratives to diversified sector growth is real, and the numbers back it up. According to the African Development Bank’s 2026 Macroeconomic Performance and Outlook report, Africa’s real GDP surged to 4.2% in 2025, outpacing the global average of 3.1%, with projections stabilising at 4.3% in 2026. Foreign direct investment rebounded sharply in 2024, rising by more than 75% to reach $97 billion. These are not numbers from a fragile or peripheral market. They represent a continent with structural tailwinds that are only strengthening.

The fundamentals are hard to ignore. Africa’s population is expected to surpass 2.5 billion by 2050, and the continent currently holds the world’s youngest median age. That demographic reality creates enormous consumer demand in everything from food and healthcare to mobile services and housing.

Urbanisation is accelerating the effect. Cities like Lagos, Nairobi, Accra, and Cairo are evolving into economic hubs with growing middle classes, increasing purchasing power, and demand for modern infrastructure. The African Development Bank estimates that over 350 million Africans are now part of the middle class, and that number is climbing.

Meanwhile, digital adoption is leapfrogging older systems entirely. With over 600 million mobile users across the continent, Africa has become a global leader in mobile-based financial services, creating an ecosystem where technology solves infrastructure gaps rather than waiting for them to be filled. The African Continental Free Trade Area (AfCFTA), which aims to unify a market of over 1.4 billion people, is also reshaping cross-border trade and investment flows in ways that are still unfolding.

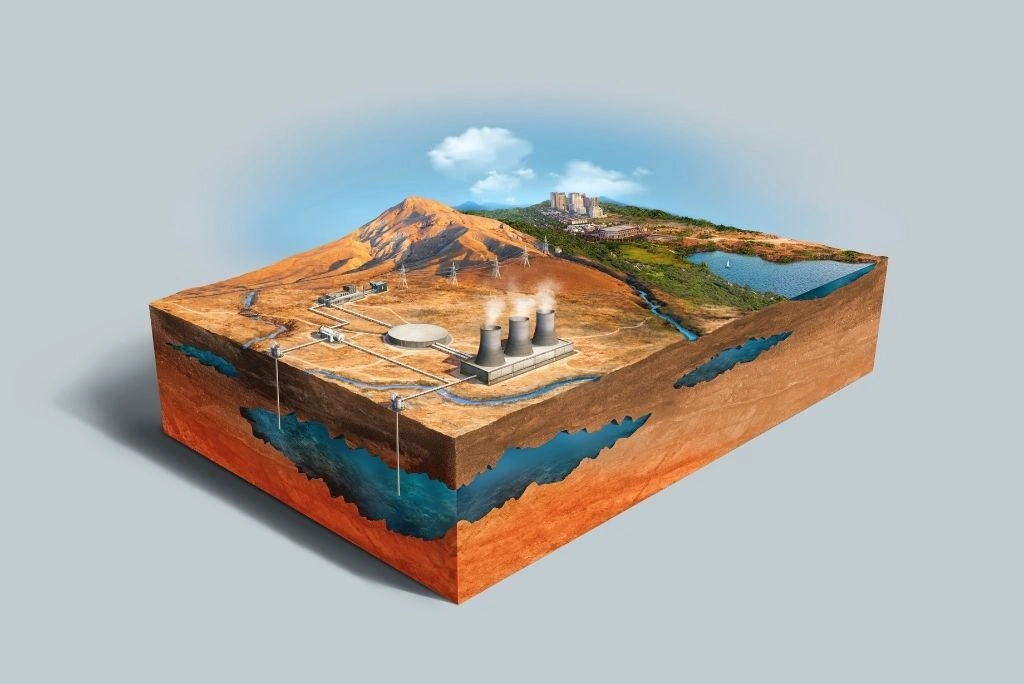

Africa holds roughly 60% of the world’s solar potential, yet the continent accounts for only about 3% of global energy investment. That gap represents one of the most compelling structural imbalances in global finance today. Over 600 million people on the continent still lack access to reliable electricity, a figure that underscores both the scale of unmet need and the size of the addressable market.

Renewable energy investment in Africa has been accelerating meaningfully. In 2025, the continent secured $13.84 billion across 306 energy transition deals, with clean energy projects accounting for 98.3% of total investment value. The African Development Bank, World Bank, and private institutions like Standard Bank were among the top investors driving that figure.

Landmark projects are setting the tone. Egypt’s Benban Solar Park (1.5 GW) and Morocco’s Noor Ouarzazate Solar Complex, which supplies electricity to over 2 million people while offsetting 700,000 tonnes of CO2 emissions annually, are now continental benchmarks. The AfDB and World Bank’s Mission 300 initiative, launched in early 2025, is targeting electricity access for 300 million Africans by 2030, mobilising billions in public and blended finance alongside it.

Green hydrogen is also entering the picture. Mauritania’s green hydrogen project alone is expected to generate roughly $34 billion in investment over its lifecycle. For impact investors, ESG-aligned funds, and long-horizon infrastructure capital, renewable energy across sub-Saharan and North Africa represents one of the most scalable and underpriced opportunities on the planet.

Africa’s fintech ecosystem is not a trend. It is a structural transformation built on the reality that traditional banking never adequately reached most of the population. With 57% of sub-Saharan Africa’s population still unbanked, the opportunity to build financial infrastructure from scratch using mobile technology is enormous.

Mobile money services, digital lending platforms, and cross-border payment systems have already demonstrated outsized returns. In peak funding years, African startups raised over $6 billion, and early-stage fintech returns have regularly exceeded 20% IRR in well-positioned markets. Nigeria, Kenya, Egypt, Ghana, and Senegal are the current epicentres, but the pipeline extends much further as connectivity improves across West and East Africa.

The regulatory environment is maturing. Regional frameworks for digital identity and interoperable payment infrastructure are advancing, which matters for institutional capital that needs compliance clarity before deploying at scale.

Africa holds 65% of the world’s uncultivated arable land, yet the continent imports a significant portion of its food needs. That structural inefficiency is an opportunity. Agritech companies are using satellite data, precision inputs, digital market access, and mobile advisory tools to transform smallholder productivity across the continent.

The AfDB’s African Emergency Food Production Facility, which mobilised $1.5 billion to help around 30 countries expand cereal and staple production, demonstrated just how quickly capital can translate into output gains when properly deployed. Soybean yields in Burkina Faso, for instance, rose from 900 kg per hectare to 1.6 tonnes per hectare under one coordinated programme. Global food production needs to increase by 50% by 2050, and a large portion of that capacity will need to come from Africa.

Transport corridors, port modernisation, urban housing, water systems, and road networks are all chronically underfunded across the continent. The AfCFTA will only amplify this demand, as intra-African trade requires physical infrastructure to flow efficiently.

In November 2025, the European Investment Bank and the African Development Bank signed a $275 million agreement to modernise Mauritania’s main railway corridor. Greenfield investments in logistics and manufacturing are rising, particularly in East and North Africa. Infrastructure remains one of the most capital-intensive but also most strategically essential sectors for long-term investors with patient capital.

Africa’s healthcare market is projected to reach $259 billion by 2030. Despite this scale, the continent imports a substantial share of its pharmaceuticals and medical devices, which points directly to where the manufacturing and distribution opportunities lie.

Governments across the continent are increasingly supporting domestic pharmaceutical production through direct incentives, making local manufacturing one of the more policy-backed plays in the sector. Healthtech startups offering telemedicine, diagnostics, and insurance products are scaling in parallel, particularly in the larger urban centres.

Digital commerce is expanding rapidly, but the infrastructure to support it has not caught up. Last-mile delivery, cold chain logistics, warehouse management, and payment settlement systems are all areas where significant private capital is being deployed and where operators with strong local networks have considerable advantages.

Digital infrastructure underpins almost every other sector on this list. Broadband expansion, data centre development, fibre connectivity, and cloud services are all areas attracting consistent FDI, particularly in Nigeria, Kenya, Egypt, South Africa, and Ghana. The digital economy now leads all new FDI project announcements across the continent.

The sectors drawing the most capital tend to share a few characteristics. First, there is a clear demand gap that will not close on its own without investment. Energy access, financial inclusion, food security, and healthcare all fall into this category. Second, digital adoption across Africa means that technology-enabled models can scale faster and more cheaply than traditional infrastructure approaches. Third, government support through special economic zones, tax incentives, power purchase agreements, and AfCFTA-related reforms is increasing. Regional initiatives add another layer, with blended finance instruments de-risking entry points for private capital.

Honest sector analysis cannot ignore the friction points. Infrastructure gaps remain significant, and while they create opportunity, they also add cost and execution risk to operations. Regulatory inconsistency across 54 different markets means that frameworks applicable in Kenya may not translate to Cameroon or Zambia. Currency volatility, particularly in Nigeria and Egypt, creates real exposure for investors without effective hedging strategies. Political risk, concentrated in parts of West and Central Africa, requires careful due diligence and local partnership structures.

Debt distress is also a consideration. Over 20 African countries are currently at elevated risk of, or already in, debt distress, which can constrain public sector co-investment capacity. None of this makes Africa uninvestable. It makes it a market that rewards preparation, local knowledge, and long time horizons.

Africa is not one market. It is 54 distinct economies with varying regulatory environments, growth trajectories, sector strengths, and risk profiles. North Africa, led by Egypt and Morocco, has deepening ties with European capital and advanced renewable energy pipelines. East Africa, with Kenya and Ethiopia as anchors, is strong in fintech, agritech, and logistics. West Africa’s Nigeria and Ghana are digital and consumer market heavyweights. Southern Africa, anchored by South Africa, offers more developed capital markets. Investors approaching the continent without this granularity will consistently misread both the risk and the opportunity.

Over the next decade, the sectors with the strongest compounding growth stories are renewable energy, fintech, agritech, and digital infrastructure. These align directly with Africa’s demographic reality, its infrastructure deficit, and the global capital flows now prioritising ESG and sustainability mandates. Technology will act as a multiplier across all of them.

The investment opportunities in Africa are no longer an emerging market narrative reserved for frontier-focused funds. They are becoming mainstream. With Africa’s GDP growth projected to hold at 4.3% in 2026 and climb further through the decade, and with the AfCFTA progressively deepening intra-African trade, the structural case for long-term exposure across multiple sectors has never been stronger. The window for early-mover positioning remains open, but it is narrowing.

Disclaimer: This content is for informational purposes only and does not constitute financial, investment, or legal advice. Investment conditions and sector performance may vary significantly across African countries and industries. Readers should conduct independent research and consult qualified professional advisors before making any investment decisions.

Sources

1. African Development Bank (AfDB) Africa’s Economic Resilience Holds Firm Amid Global Headwinds – 2026 Macroeconomic Performance and Outlook (MEO) Report

2. African Development Bank (AfDB) 2026 Annual Meetings: AfDB Group Boosts Co-Financing to Scale Up Investments Across Africa

3. African Development Bank (AfDB) Mission 300 – Africa Energy Forum 2025

4. African Development Bank (AfDB) Africa’s Macroeconomic Performance and Outlook 2026 – Full Report

https://www.afdb.org/en/documents/africas-macroeconomic-performance-and-outlook-2026

5. Ecofin Agency Africa Attracted $13.84 Billion in Energy Transition Investment in 2025

6. International Renewable Energy Agency (IRENA) A Just Energy Transition for Communities: Large-Scale Wind and Solar Projects in Sub-Saharan Africa (2025)

7. FurtherAfrica Africa’s Development Crossroads: Progress, Challenges, and Opportunities in 2025

8. FurtherAfrica Five African Countries to Watch for Investment in 2026

https://furtherafrica.com/2025/08/04/five-african-countries-to-watch-for-investment-in-2026/

9. African Market Insights (Beehiiv) Africa’s FDI Is Concentrating in Specific Growth Sectors: Renewable Energy and Technology

10. Institute for Security Studies (ISS) – African Futures Africa Financial Flows Forecast

https://futures.issafrica.org/thematic/10-financial-flows/

Renewable energy, fintech, agriculture, healthcare, and digital infrastructure are currently the strongest sectors driving investment opportunities. These areas combine large unmet demand, growing digital adoption, and increasing government support, making them attractive across multiple markets and risk profiles.

Africa holds roughly 60% of the world’s solar potential, yet over 600 million people still lack reliable electricity access. That gap, combined with maturing green financing tools and major institutional backing like the AfDB-World Bank Mission 300 initiative, is driving rapid growth in renewable energy investment in Africa. In 2025 alone, the continent secured $13.84 billion across 306 energy transition deals.

Yes, and it remains one of the most underrated investment opportunities. The continent holds 65% of the world’s uncultivated arable land, productivity is low relative to potential, and agritech is actively closing that gap. With global food demand projected to rise 50% by 2050, agriculture offers strong long-term returns, especially when paired with technology and local operational knowledge.

Africa’s tech sector is maturing fast, shifting from rapid expansion toward profitability, consolidation, and deeper infrastructure. Fintech revenues are projected to grow from $10 billion today to over $65 billion by 2030, while AI is expected to add $2.9 trillion to the continent’s economy over the next five years. The fundamentals, a young population, expanding connectivity, and growing homegrown capital, make tech one of the most compelling long-term plays on the continent.

Based on UNDP investment data, fintech and financial services consistently show the highest ROI profiles, with virtually all assessed opportunities projecting returns above 15%. Renewable energy and agriculture follow closely. Early-stage fintech investments in markets like Nigeria, Kenya, and Ghana have regularly exceeded 20% IRR. As any honest Africa sector analysis will show, returns vary significantly by region, so sector and geography need to be evaluated together.

Renewable energy projects backed by long-term power purchase agreements, healthcare, and digital infrastructure tend to offer the most resilient return profiles. These are among the sectors attracting investments with the most stable demand, regardless of short-term economic cycles. Pairing sector selection with strong local partnerships and markets with sound regulatory environments, such as Rwanda, Morocco, and Kenya, further reduces risk considerably.

Africa is not the same continent it was a decade ago. The narrative has shifted from aid dependency to innovation hubs, from risk-heavy frontier markets to high-growth investment destinations attracting serious capital. Business opportunities are multiplying at a pace that even seasoned investors are scrambling to keep up with, driven by a young population, accelerating […]

A decade ago, conversations about investing in Africa rarely moved beyond oil fields, mining concessions, and commodity cycles. That framing was always incomplete, and today it’s simply outdated. Africa’s economic development has entered a new phase, one defined less by what sits beneath the ground and more by what is being built above it: cities, […]

When Global Capital Started Taking Africa Seriously Something shifted in how the world sees African startups. It was not a single moment. It was a series of signals. A Nigerian fintech processing hundreds of millions of transactions monthly. A Kenyan pay-as-you-go energy company financing smartphones and solar panels for people who had never held a […]